What is the maximum Solo 401k contribution for 2020?

John Kim

Published Apr 26, 2026

Hereof, how much can I contribute to my Solo 401k?

The maximum amount a self-employed individual can contribute to a solo 401(k) for 2019 is $56,000 if he or she is younger than age 50. Individuals 50 and older can add an extra $6,000 per year in "catch-up" contributions, bringing the total to $62,000. (Amounts are higher for 2020.)

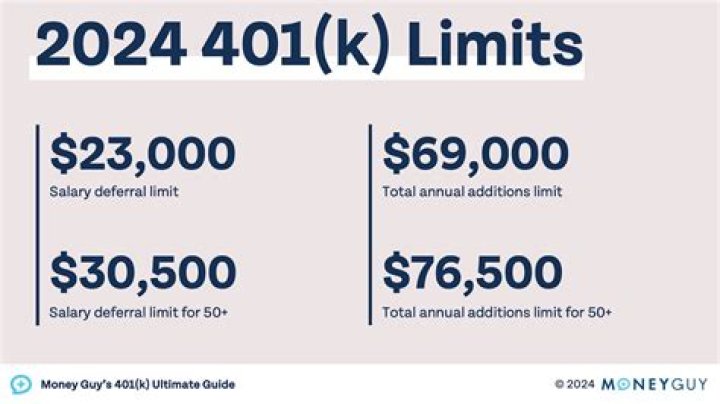

Subsequently, question is, what is the max 401k contribution for 2020? The amount you can contribute to your 401(k) or similar workplace retirement plan goes up from $19,000 in 2019 to $19,500 in 2020. The 401(k) catch-up contribution limit—if you're 50 or older in 2020—will be $6,500 for workplace plans, up from $6,000.

Keeping this in consideration, what is the maximum 401k contribution for 2020 for over 50?

Highlights of changes for 2020 The catch-up contribution limit for employees aged 50 and over who participate in these plans is increased from $6,000 to $6,500. The limitation regarding SIMPLE retirement accounts for 2020 is increased to $13,500, up from $13,000 for 2019.

Can I contribute to both employer 401k and Solo 401k?

In this case, you are eligible to contribute to both the employer-sponsored 401k and the Solo 401k. Regarding the contribution limit, the salary deferral portion is per person, not per plan. You need to split this between your Solo 401k and the regular 401k account.

Related Question Answers

Does Solo 401 k reduce self employment tax?

The only guaranteed way to lower your self-employment tax is to increase your business-related expenses. Above-the-line deductions for health insurance, SEP-IRA contributions, or solo 401(k) contributions will not reduce your self-employment tax, either. These deductions only reduce the federal income tax.Who offers Solo 401k?

6 Best Solo 401k Providers- TD Ameritrade Solo 401(k)

- Fidelity Solo 401(k)

- Vanguard Solo 401(k)

- Charles Schwab Solo 401(k)

- E-Trade Solo 401(k)

- Rocket Dollar Solo 401(k)

Who can open solo 401k?

In order to make annual solo 401k contributions, you must be self-employed with no full-time W-2 employees and the contribution has to be based on earned income generated from your self-employed business; therefore, no alimony payments can not be used to make annual solo 401k contributions.Can I set up a Solo 401k?

Solo 401(k) Costs Setting up a Solo 401k plan is now easy, simple, and cost effective. You can use the new IRA Financial app to set up a Solo 401(k) on your own.Can I have a simple IRA and a solo 401k?

If you have not, do not make it to the SIMPLE IRA if the SIMPLE IRA is also for your self-employed business, as the IRS rules do not allow contributions in the same year to both a solo 401k and a SIMPLE IRA.Can you have 2 Solo 401k plans?

ANSWER: Yes you can contribute to both your solo 401k plan and your IRA in the same year. However, the IRA contributions may not be fully tax deductible since you are also contributing to a solo 401k plan.Where do you deduct Solo 401k contributions?

Instead, the IRS detailed that the individual should have deducted the plan contribution on line 28 of Form 1040. This is the same line that Solo 401k or Individual 401k contribution is deducted. Line 28 is titled “Self-employed SEP, SIMPLE, and qualified plans.”Can a solo 401k have a match?

do I need to make equal solo 401k contributions for me and my wife or can they be different? Because a solo 401k plan is only for owner-only businesses, equal contributions do not apply; therefore, just one spouse can contribute while other does not.How much can I put in my 401k if I am over 50?

The maximum amount workers can contribute to a 401(k) for 2020 is $500 higher than it was in 2019—it's now up to $19,500 if you're younger than age 50. If you're age 50 and older, you can add an extra $6,500 per year in "catch-up" contributions, bringing your total 401(k) contributions for 2020 to $26,000.How much can you contribute to a 401k if you are over 50?

There are annual limits. In 2016, if you are under 50 years old, you can contribute a maximum of $18,000. If you're 50 or older, you can make an additional catch-up contribution of as much as $6,000, for a total of up to $24,000. Those contribution limits change annually to track inflation.What is the over 50 catch up for 401k?

For those employees aged 50 and over who participate in 401(k), 403(b), most 457 plans, along with the federal government's Thrift Savings Plan, this catch-up rate is $6,500 for 2020 ($6,000 for 2019). For SIMPLE 401(k) plans, the catch-up contribution remains is $3,000 for 2019 and 2020.Can I make a lump sum contribution to my 401k?

Although you can't boost your 401k account by adding cash into it whenever you like, you might be able to increase your paycheck contributions for free. If you can't change your contribution percentage or you don't have a 401k account, IRA accounts and bonds should be your next choice.What happens if I contribute more than 19000 to my 401k?

According to the IRS, if you overcontribute to your 401(k), you'll have until April 15 of the next year to correct the problem. The excess amount taken out is then included in your gross income for the year in which it was contributed to the 401k, according to the IRS.How much should I have saved for retirement by age 55?

Experts say to have at least seven times your salary saved at age 55. That means if you make $55,000 a year, you should have at least $385,000 saved for retirement. Keep in mind that life is unpredictable–economic factors, medical care, how long you live will also impact your retirement expenses.How much can a highly compensated employee contribute to 401k?

Those married filing jointly can contribute up to $19,000. Single filers can contribute up to $19,500 in 2020. If you're at least age 50, you can direct an additional $6,000 in “catch-up” contributions. The catch-up contribution for 2020 is $6,500.Should you max out your 401k?

When you should max out your 401(k) You may want to consider maxing out your 401(k) if: You earn a lot and want to reduce your tax bill. You want to give compound interest a chance to help your money grow, tax-deferred. You've achieved some of the important non-retirement goals we've outlined above.How do you max out your 401k?

Tips for maxing out your 401(k)- Take it slowly. Start by saving, then increase your rate when you get raises and whenever it's feasible.

- Choose automation over budgeting. The Principal survey found that 70% of retirement super-savers don't use a budget.

- Believe in your money smarts.